Presented by

David Laibson

Robert I. Goldman Professor of Economics, Harvard University

with discussants

William Goetzmann

Edwin J. Beinecke Professor of Finance and Management Studies, Yale School of Management

Jan Svejnar

Member, Committee on Global Thought

Director, Center on Global Economic Governance

James T. Shotwell Professor of Global Political Economy, School of International and Public Affairs, Columbia University" />

Long-Term Investing: An Optimal Strategy in Short-Term Oriented Markets

December 3, 2012

Long-Term Investing: An Optimal Strategy in Short-Term Oriented Markets

Paper Presentation III: “Natural Expectations, Macroeconomic Dynamics, and Asset Pricing,” (Fuster, Herbert & Laibson, 2011)

- David Laibson, Robert I. Goldman Professor of Economics, Harvard University

Discussants:

- William Goetzmann, Edwin J. Beinecke Professor of Finance and Management Studies, Yale University

- Jan Svejnar, James T. Shotwell Professor of Global Political Economy, School of International and Public Affairs, Columbia University

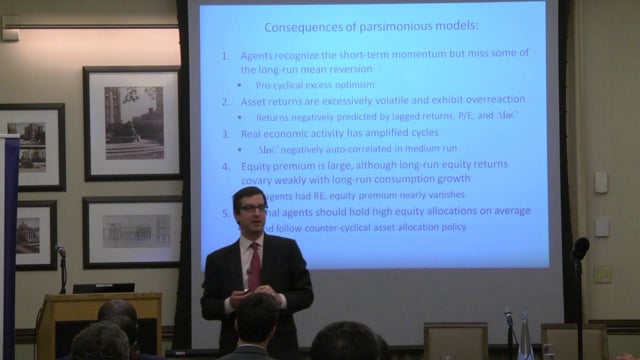

David Laibson explored the impact of under-estimating long-term mean reversion, demonstrating the effects on asset pricing, consumption and excess returns.

Read the transcript of this event: Laibson, Goetzmann, Svejnar, Natural Expectations

Part of the Sustainable Investment research initiative.